Before I begin this blog, I want to say that every financial product is created with good intention to help a subset of people. The issue in the financial industry becomes when that financial product begins to get sold to the masses versus the intended sub group it was built for. This happens a lot in the insurance industry due to the commissions received on many of these products. With that being said, let’s break life insurance down.

Life insurance is a Must. When people ask me whether or not it is necessary to have insurance, I am always a bit confused. The word in and of itself tells us what it is. Insurance is protection; it is peace of mind. It is protection for when something happens. Believe me, things do happen. I know all too well that things happen. So, do we need insurance? It is a resounding yes! You need insurance especially if you have dependents UNLESS you are independently wealthy and money is of no consequence. So, if you have dependents and need to insure compensation for them if you incur any kind of illness and when you die, you need to have life insurance. However, how much and what kind are really the more specific questions people should ask.

How much insurance is relatively easy to answer. Most financial advisors will tell you to have between ten to twelve times your yearly salary. If, for example, you are making $100,000.00 a year, you would need about one million dollars worth of life insurance for your dependents. It is easy math: $100,000.00 X 10 = $1,000,000.00. Think about your lifestyle to determine if you feel more comfortable with ten, eleven, or twelve times your salary. But the point is that your spouse would be able to invest the payout sum and live off of the returns from that investment.

The more important and confusing question is not whether you need insurance or the amount you need, but what kind of insurance. There are different types of insurance that you can get and many insurance agents will try to coerce you into believing you owe it to your spouse and family to be over insured. Remember, that is how insurance agents make their money. Don’t fall prey to getting more insurance than you need. You are simply paying the agent more commission than is necessary. So be wary and know what type of insurance you need before having the conversation with any agent.

Basic Types:

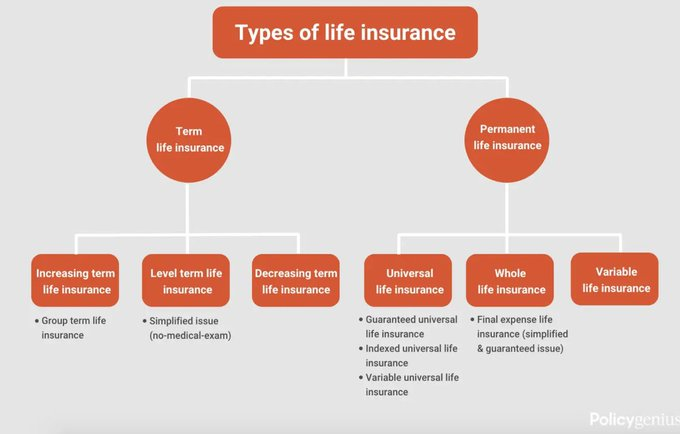

There are two basic types of life insurance: permanent life and term life. There are several types of insurance that fall under permanent life. But before discussing the varieties of permanent life insurance, let’s delineate the fundamental differences between permanent life insurance compared to term life insurance.

Permanent Life Insurance:

Permanent life insurance is something to really think about before buying it. It is rather confusing and expensive. Life insurance is not supposed to be a savings account but is life insurance to replace your income when you die. Permanent life insurance is insurance that has an investing component to it. It is life insurance that you purchase for your entire life and pay through monthly premiums which are supposed to grow as an investment over the span of your life. This amount changes as you age. Also, the money grows at a very slow rate. You are not getting a good return on your money. In addition, it is much more expensive than term life insurance, ranging anywhere from five to fifteen times higher. Another negative aspect of permanent life insurance is its complexity. Unlike term life insurance, not only are there premiums that you pay for your whole life, but you often also have to pay fees and taxes. There are also other stipulations that can be associated with it. Something that can’t be dismissed, however, is that there is a cash value associated with it. Some people choose to take some of the cash before death, thinking of it as a savings account. Be careful. Remember what the intent of insurance is. So taking part or all of the accrued amount before death may not leave your loved ones with the necessary money once you die.

Term Life Insurance:

Term life insurance is quite different from permanent life insurance. Term life insurance is limited to the amount of time you select. You get to determine the length of time you are covered, and you pay premiums for that span of time. It does not cover you for your entire life span like permanent life insurance does. In addition, it pays a specified amount when you die. It does not incur interest like permanent life insurance does, nor does it pay after the term if you die after the term of the insurance contract. However, with term life insurance, you determine the length of time you think you need the insurance and the amount of payout necessary for your family when you die. The amount you need was noted above. The premiums for term life insurance are relatively low. Insurance companies use an amortization chart to determine the premiums based on your age, health, amount of death benefit, and the length of the term. Like permanent or whole life insurance, there are several different types of term life insurance that we will delve into to give you a better understanding of your options.

Types of Each Category:

Let’s take a look at the different types for each of the two categories of life insurance to give you a better understanding, so you can best determine what will fit your needs. With permanent life insurance, there are many different types from which to choose. A few of the more common types of permanent life insurance are:

- Universal life insurance which includes indexed universal life insurance

- Guaranteed life insurance

- Variable universal life insurance

- Whole life insurance which includes final expense insurance both simplified and guaranteed

- Variable life insurance

There are many other permanent life insurance plans that you can find such as group life insurance and accidental death and dismemberment life insurance. But for the most common ones that are noted, there are some definite considerations to keep in mind. Like permanent life insurance, term life insurance also has several types of policies. The most common are: increasing term life insurance, level term life insurance, and decreasing term life insurance. Each of these has things to keep in mind before deciding what kind of term life insurance policy is best for your needs.

Universal Life Insurance:

The basic premise behind any type of universal life insurance is that it is insurance that will secure your family’s future when you die and will grow your money over the course of the life insurance span. Many people fall prey to this trap, thinking that their money will grow at a fast pace, leaving their family well off when they die. That is NOT actually the case. However, it is insurance for your family, so they will benefit from you having some kind of insurance. The pitfall is in thinking the money will grow to be some kind of windfall. While all universal life insurance plans have definite drawbacks, they differ from plan to plan.

- Indexed universal life insurance – Be aware that the cash value, despite what you may be told, has a minimum and a maximum guaranteed interest rate which is based on a stock market index. The value in having this type of insurance is that there will be some cash gain over and above your premiums. Just know that there is a cap on the amount of increase which is based on the participation rate. Your policy will determine how much your cash value “participates” in the gains. An example is that if your participation rate is 80% and the S&P 500 goes up 10%, you will only get an 8% return. Also, there is a cap on the gains. Therefore, if the index increases 20% and your cap is 10%, you will only get a 10% return. Also, some policies will have flexible premiums and death benefits that will let you adjust your death benefit as the needs of your family changes. Another aspect of this insurance is that you may skip a payment or may even be able to decrease your premiums within limits but only as long as the amassed cash value covers the costs. However, if you skip payments and don’t have enough cash value to cover the cost of the premiums, your policy could lapse. An indexed universal life insurance policy is probably best for someone who has maxed out other investment accounts and is looking for additional investment flexibility or someone who is looking for a safe investment with guaranteed minimum values.

- Guaranteed life insurance – Another kind of universal life insurance plan is a guaranteed life insurance policy. Because it is “guaranteed,” the money accrued in it is stable. Also, the premiums remain the same regardless of how the market indexes perform. However, there is not a guaranteed cash value amount with this type of policy and missing any payments may forfeit the entire policy. This kind of universal life insurance is best for those who are risk-averse people who have permanent insurance needs.

- Variable universal life insurance – The third type of universal life insurance is a variable universal life insurance policy which has a benefit of cash value gains. The way this works is that the money that the policyholder pays as premiums goes into a series of mutual fund sub accounts. Because the money is in these funds, there is a savings potential and the policyholder also has the ability to borrow against the policy. A major negative of this plan is that the policyholder manages the investment portfolio. For some, this may be okay, but for the masses or those who are not financially savvy, this may be a mistake. In addition, since the policyholder can borrow against the policy, those interested in this type of policy must be disciplined to ensure the money needed for the family will actually be there at the time of death. Other negatives associated with variable universal life insurance policies are that the cash value and actual death benefit can fluctuate based on performance as well as the fact that there are high fees associated with these policies. This type of policy is only good for do-it yourself investors who tolerate risks.

Whole Life Insurance:

Let me start by saying I am not a fan of this type of life insurance for MOST people. According to Forbes, this was one of the most popular types of life insurances in the United States for most of the 90s, and it is still fairly popular, representing “33% of total life insurance premiums” as reported “‘from LIMRA, an industry-funded research group.’” Whole life is supposed to be just that, insurance that covers you for your whole life, having guaranteed premiums, cash values, and death benefits. Sounds somewhat appealing, right? Well, know that some whole life insurance policies actually have a limited, and, therefore, higher premium and the cash values or dividends grow very slowly. In addition, not all whole life insurance policies pay dividends. So, be careful when selecting between participating whole life insurance policies and non-participating whole life insurance ones that do NOT pay a dividend and are offered by stock insurance companies rather than mutual insurance companies. For those that are participating whole life insurance companies, you usually have the option when it comes to your dividends. These options typically include putting the dividends toward your life insurance premiums, taking the dividends as a cash payout, or using it toward life insurance additions. My biggest problem with this type of insurance is that it is more expensive with term life insurance policies, and it negates the purpose of life insurance. Life insurance is not meant to be a savings or investment account, so I prefer to keep those two things separate and not have to pay as much for the insurance. I think you should not fall prey to the gimmicks associated with this type of insurance.

Variable Life Insurance:

Another type of insurance that is available, but another one I do not endorse, is variable life insurance. This type of insurance can be very risky. It is a life insurance policy that some use for life insurance needs as well as investment needs and goals. The intended purpose of this insurance is to pay a certain amount of money to your beneficiaries when you die along with having a cash value. These amounts are all determined by your selected premiums but also have attached to that fees and expenses. One huge downside is that the cash value is dependent upon the performance of the funds in which your money is invested. If the market is underperforming, you will lose some or all of the cash value. Additionally, there are fees that come out of the premiums and are paid to the financial professional. As I have already noted, I think insurance needs should be just that – just insurance and not savings or investments.

Term Life Insurance:

As noted above, unlike permanent life insurance or whole life insurance, term life insurance does not have a cash value associated with it, so it is only insurance and not a savings plan. It is more simplistic than permanent life insurance. In basic terms, term life insurance is nothing more than a contract between the policyholder and the insurance company stipulated for a certain amount of time, “the term,” that will pay the agreed amount of the policy to the beneficiary or beneficiaries at the time of death of the policyholder. One of the benefits of term life insurance policies is that they are affordable, usually five to fifteen times cheaper than permanent life insurance. In addition, you get to determine the “term” which typically ranges from one to thirty years. A downside is that the predetermined term often expires before death. If the policyholder wants to get a new policy, the cost at a later point in the person’s life is more expensive than the original policy.

- Increasing term life insurance – This type of term life insurance is one that has an added benefit of having a death benefit that increases over the term of the policy. In addition, the policy can have varying premiums if that is something the policyholder determines when establishing the policy. One caveat, however, is that this type of term life insurance is usually more expensive than other policies.

- Level term life insurance – This is the most common type of term life insurance for several reasons. First, it has a fixed price which most people prefer for budgeting reasons. Next, it is straightforward. The basics of this type of term life insurance is that there is a set premium and a preset death benefit. It is that simple. For most people, this is the best type of term life insurance.

- Decreasing term life insurance – As the name suggests, this form of term life insurance has a death benefit that decreases over the span of the policy. It does have a set premium like level term life insurance. This is the type of insurance a policyholder may desire until debts are paid. Often as we age, our salaries increase and we pay off debt, so we need to be less insured than when we are first starting out, have less income and more debt. In that case, we need to ensure that our loved ones are secure in the event of our death. For those individuals, this type of insurance may be of interest. Many who purchase this type of term life insurance do it as a safeguard until the mortgage is paid in full. This is often suggested and purchased through your mortgage lending company or bank.

ALL INSURANCE:

Overall, some kind and type of insurance is necessary. Remember the premise for the insurance; it is just that – protection. You need to safeguard your family in the event that tragedy strikes. Think about how vulnerable your spouse and/or family would be if that happened. Imagine how catastrophic it would be if they had to worry about not being able to pay the bills or stay in the family home. Protect them from those worries. You have the information to make an education decision regarding which of the two basic kinds of insurance would best fit your needs as well as what particular type. One thing I ask of you is not to wait. This is definitely something you cannot put off. Don’t be caught off guard. It is not very expensive and the peace of mind is priceless.