Believe it or not, it’s November and that means the holidays are fast approaching. Just walk into ANY store and you will not be able to miss the explosion of holiday décor, food, gift-sets, wrapping paper, etc. It amazes me how many people from year-to-year seem to be caught off guard as if the dates of the holidays change. Nonetheless, we all know from Halloween until New Year’s, it is a whirlwind of activities, spending, and stress. So while the holidays are supposed to be fun and a time for gathering with family and friends, people will feel undue and other self-induced levels of stress. Information published by Clarity Clinic in 2021 noted that of those surveyed, “45% of those people living in the United States would choose to skip out on the holidays” to eliminate the stress that comes with it. One of the biggest contributors to this feeling of stress is money. In fact, according to a poll conducted by the American Psychological Association, “69 percent are stressed by perceiving a ‘lack of money,’ and 51 percent are overly stressed by the ‘pressure to give or get gifts.’”

So what can be done to help alleviate some of the stress about money and, instead, really enjoy the holidays? First, stick to your budget. The holidays are not about wrecking your budget and then having to struggle to pay off holiday bills until the summer rolls around. Take a step back and think about what the holidays really are all about. Keeping in mind that the purpose of the holidays is to gather with family and friends, it does not have to become an over the top spending and gift giving frenzy and fiasco.

Also, keep things real and be honest. It is fine to have a conversation with your family – immediate and extended – about your budget and your financial goals you are working toward. Chances are others may even be relieved to remove some of this burden as well. Your family should support your efforts to pay off your debts, save for a house, stay on a budget, or whatever your budgeting focus is. However, if gift giving is something that is really important to you and your family, keep it in check and make sure you budget for it well in advance. It is much easier to set aside a certain amount each week, biweekly, or monthly, ahead of time rather than having to come up with all of the money for decorating, gift giving, and entertaining beginning in November or December. Hopefully you worked this into your budget before the holidays were looming over you, but there are also things to help you enjoy the holidays and stay on a budget, especially if you didn’t.

Entertaining: Entertaining will definitely cost more this year, so you will want to plan ahead to find the best bargains. The Farm Bureau’s 36th annual survey notes that there will be a “14% increase from last year’s average of $46.90 for a classic Thanksgiving dinner for ten.” Christmas will likewise be more expensive due to continually rising food costs. So, you know the cost is going to be higher which you need to account for when setting up your November and December budgets. In addition, watch the ads and shop around. Grocery stores will have key items on sale to bring in the crowds. Remember that you don’t always have to buy the most expensive brands. Many of the store brands are equally as good, yet less expensive. Another budgeting tip is to have everyone bring something to the meal. Spreading the expense helps everyone. Plus many people enjoy bringing a new or favorite food item. Lastly, keep it simple and remember you do not have to have the “traditional” meal. Don’t buy into all of the hype. Do your own thing. It is okay! This will also cut down on the stress level of having to do too much as well as the stress of blowing your budget. Lastly, live in the real world rather than trying to create a Thanksgiving meal that is straight from the pages of a magazine or some Pinterest post. Keep it uncomplicated, so you can spend more quality time with your guests rather than trying to create something that is overdone and excessive.

Decorating:Just like entertaining, decorating does not have to be some major expense. Personally, I am a pretty simple guy and don’t put much stock in this. I also don’t buy into all of the hype dictated by big companies trying to tell me I need to do this or buy that in order to be happy or to be able to have a good holiday. It is not how I roll. For my wife and me, I can honestly say the more we simplify our lives and go against the norm, the happier we are. But if you so choose and feel the need to decorate, there are many discount places that have decorating items that you can buy that will keep your budget in tact. Again, keep in mind what is important. Assess your plan. Is it really necessary to have things decorated to the nines or can you use what you already have? Is it really that important to you or is sticking to your budget and paying off your debt more paramount? Maybe this is another time to keep things simple and understated. You may find that this is also a wonderful way to reduce stress and to free up your time. Keeping in mind the real focus of the holidays will help you here. Often a candle or two, some greenery that you can usually get free from places that give a fresh cut to Christmas trees, and a plate of cookies or an appetizer is really more than enough. Lastly, planning ahead and buying wrapping paper and other “necessary items” after the holidays for the next year when the stores discount it is a good way to save money. Just make sure you buy ONLY what you need. It is not going to help your budget if you buy more than you need just because it is on sale. That is not being frugal or staying on a budget. .

Gifts: If it is a must to give gifts, see how you can tapper back. As you can imagine, I am not into “stuff,” so I don’t need or want others to buy me gifts. Obviously, this is a personal thing and clearly children are a different consideration. How do you feel about gifts? Instead of buying things to fill a quota or a dollar amount, get creative. Are there things you can do for the person rather than give to him or her that would be equally or more appreciated? Gifts of time and experiences are usually valued far more than tangibles that eventually break, are shoved in the back of the closest, or are thrown out. Really think about the person. What does that individual treasure? Food items are a great gift and can be made fairly inexpensively. For example, collecting all of the dry ingredients for cookies, muffins, brownies, or gourmet hot chocolates and putting them in a Ball jar with the directions is a gift that is economical and thoughtful. Often you can make several of these gifts, marking many people off your list while also keeping you out of crowded stores filled with cranky last minute shoppers. It is the thought that is important – not the cost. Another fairly inexpensive and very thoughtful gift is tickets to a movie with the promise to care for little ones for a needed date night. The list is endless. You don’t have to break the bank if you are innovative. However, maybe it is time to stop giving and begin new traditions. One that my wife’s family started several years ago was everyone bringing a new game to share that we then played that night. Every couple also brings an appetizer, so it is really just a relaxing evening that is not overly complicated. Think outside of the box. Dare to break away from the norm and don’t buy into believing that you have to do things that are not good for you and your situation.

Bottomline, the holidays are meant to be time to gather with family and friends. Refuse to buy into all of the hype and commercialism. It is not helping you financially, emotionally, or personally. Take stock in what is important and stick to that. Celebrate the holidays in the way they really should be celebrated. To me that is simplistic, stress free, and with the people I value most in my life.

I am often asked about my success and what my special recipe is or the secret elixir to create success. I wish I could attribute it to something innovative or profound. But that is not the case. Truly, my success comes down to two key things: consistency and laziness.

While many can understand how consistency plays into success, most look at me in disbelief and quizzically when I mention laziness. However, these two personal attributes really have fueled me and have helped me create my success. Let me explain how these two seemingly incompatible characteristics go together.

Outwardly I might appear to be energetic since I always seem to be busy and constantly moving. But actually I am very lazy! Sure I go to the gym and work out, clean things up because I can’t stand clutter and messes, and am task-oriented and success-driven. But when it comes to mundane minutiae, I procrastinate and am simply lazy. I know that about myself; it is not a positive attribute. Because of that, however, I automate everything, so I don’t have to deal with tedious tasks or even spend energy thinking about them. Therefore, I don’t waste time on making daily decisions about money, budgeting, investing, or finances. That is exactly how and why my laziness and consistency play into one another, creating my success.

Stepping back on my road to success, when I got really and totally consumed with my finances, I planned out everything on a spreadsheet which became my blueprint for success. This blueprint is exactly what I guide my academy students to create for themselves, so they can build their own success. Once I had everything mapped out, since I know that I am lazy when it comes to things that I consider to be trivialities, I created ways to put things on autopilot. If there was a way for me to make it one and done, I did it.

This method helped streamline and simplify my life, turning my laziness into success. That, of course, is coupled with consistency. Since I set everything up to be automated, I do not have to think about or worry about trivial matters and can focus on bigger, more important considerations. The following is the breakdown of how much time and effort I spend on each specific task with my finances.

Yearly:

Investment Allocation Rebalancing

Quarterly:

Balance Sheet Review

Monthly:

Budget – thirty minutes every month

Once (set it and assess each as needed): Remember this is NOT an excuse to constantly tinker with your plan. For example, if you have a large life event such as a birth of a child, it may be wise to reconsider insurance needs.

Plan to reach monthly goals – once decided, it is automated

Paying bills – set up to be automated and then done

Investment Accounts – set up to be automated and then done

Investment Allocations – automated and then done

Insurances – made decisions, automated and then done

Trusts and Will – made decisions and completed

Durable Health Care Power of Attorney – made decision and done

Financial Power of Attorney – made the decision and done

Tax Strategy – once decided, it was done

Investments Plan to Reach Goals – planned then automated

Investments Resources – all bookmarked on my desktop (if necessary for use)

Amortization Schedules – set up, then done until debt is paid (I have happily removed this one due to no debt.)

As you can see, I spend little to no time on these activities since they are almost all automated. Again, I am lazy when it comes to spending time doing things that are mundane and monotonous. I took my exact roadmap for success and created Budgetdog Academy to enable everyone to take this approach and free themselves from the mundane and arduous tasks of personal finance. This gives you the luxury of an automated financial plan that will take no more than a half an hour a month. You can confidently set up and automate your finances to help you reach your financial goals as well as free up valuable time. Looking at the time allotment above, you will notice that the only thing I have to spend time on each month is my monthly budget since everything else is automated. But even that is quick and easy.

This is a lazy person’s best friend! The most time consuming part is mapping out the blueprint but once you are through with this part, all you will need to do is put in a minimal amount of effort and watch the automation work.

If you are ready to take control of your finances but don’t want to waste hours a month, The Budgetdog Roadmap is your key to success. It provides every resource you need for paying off your debts, budgeting, and investing. I am always at your disposal for any questions you may have along the way. Your success fuels me, but I also feel your pains and understand your worries. Being consistent will pay off. I teach and have recreated every step that allowed me to pay off $304,000.00 of debt and reach millionaire status so that all my students can have the same success and more. My students learn to stay the course and trust the process and I even give them permission to be lazy – in a good way!

Subscribe to my Youtube as a source of the latest information for all things financial as well as some simple life lessons and inspiration. My mission is to make you successful – as many of you as I can. As long as you put forth the effort and stay with me through this journey, you will be on a great path to financial freedom and success. So what is your elixir to success? What do you want for your future? I think I know the answer. It is within your grasp; you can win.

Figures vary on the number of Americans living paycheck to paycheck with figures ranging anywhere from 58% of Americans according to information from LendingClub as reported by CNBC in June, 2022 to 64% as reported in US News and World Report. Regardless of the percentage, the numbers are staggering and many report that they are adopting this lifestyle due to the economy. This may define you. There are many “gurus” you can look to for advice such as Dave Ramsey. So, if you are one of the millions of Americans contentedly living paycheck to paycheck, you might want to stop reading this blog and just follow Dave Ramsey’s advice. But you really owe it to yourself to think about your financial situation and if Ramsey’s ideology fits your goals, needs, and circumstances.

This is not a treatise against Dave Ramsey personally. He has helped countless people figure out their financial and life situations. He even provides some sound financial advice. Despite many reviews on the Internet about Dave Ramsey and the Ramsey machine, this is not a blog railing against him. This blog is actually my take on Ramsey’s ideology and how it aligns with mine along with key elements about which I disagree. In fact, there was a time when I even contemplated working with the Ramsey group and was interviewed for a position with them. However, after the second interview, I declined in order to pursue my own path with Budgetdog.

Let’s get back to living paycheck to paycheck and advice, mine and Ramsey’s, that can help you. First, we will consider the Baby Steps that Ramsey so famously touts. In theory, I can’t argue against the Seven Baby Steps that he outlines. They are simplistic, and, when followed, they can provide a sound framework to set a person on a good financial path. For the masses, this approach makes sense. A key question, however, is how efficient are the Seven Baby Steps and how successful will the person following the steps actually be?

In order to answer that question, we need to deconstruct Ramsey’s plan and consider each of the Baby Steps. An important component to the Seven Baby Steps is that you must follow the steps in order. This is not possible or even doable for many people and is one area in which I disagree with Ramsay for several reasons. One reason is that I don’t think everyone is disciplined enough to follow the steps as stipulated. Perhaps if they were, they would not be in the financial debacle that they find themselves in thus requiring them a solution to their situation. Setting payments up to be automatically withdrawn and paid may help alleviate some of the unpredictability and natural human weaknesses and tendencies, but it doesn’t work for everyone. Moreover, I do not agree that some of the steps can’t be done simultaneously or unilaterally. Let’s go step by step to get a better understanding of what Ramsey proposes.

Baby Step One – Save $1,000.00 for a starter emergency fund:

This is one thing I personally did when my wife and I were starting out, were newly married, and were just beginning our careers. I do believe it is necessary to have some type of emergency fund in place, but I would caution against such a small dollar amount as it may not be enough for all people and in all circumstances. Thinking about many situations, this amount may only make a dent. Of course, anything will help when that “emergency situation” comes up like a major car repair or major appliance and house repairs. Your emergency fund is likely different from mine and rightly so. A one size fits all $1,000.00 is likely foolish for many.

Baby Step Two – Pay off All Debt Except Mortgage Using the Debt Snowball:

I concur with Ramsey on paying off debt and personally did this. My wife and I did this, setting up a timeline and a budget to achieve this goal in eighteen months. We were intentional and focused on paying off all our debts and actually achieved this goal in a year. I have a YouTube video on how you can also do this. Where I deviate with Ramsey, though, is that several factors need to be considered. I don’t think this can just be a blanket statement. There are things to consider such as age, goals or timeline projections for the debt pay off, current investments, available cash for investments or to pay off debts, and income. Individual goals, risk tolerance, and personal situations must also be taken into account when finances come into play. Some people may view debt as a hedge and might not make it such a priority which is not my style or mantra, but I can respect that. My recommendation, however, is to look at the debt amounts along with the amount of money wasted due to debt and make a plan to get those debts paid off in order to improve your financial situation. How you do this is a personal matter. Ramsey advocates for the debt snowball method, to pay off your smallest debt first and then move up to the largest debt. I understand the theory behind this concept because most people need to see some kind of success. Others, however, advocate for the avalanche method, paying off the debts with the highest interest rate first. You will need to assess what works best for you and go about it in a systematic and consistent manner. Furthermore, I would advise against having and using credit cards if you already have accrued credit card debt. My suggestion, like Ramsey’s, is to get rid of the credit card or cards. Simply cut them up. If they are not there, you can’t be tempted to use them, racking up even more debt. Also, think about your spending habits. Is it REALLY important to have the latest home decor at Target and are those new Nikes really going to improve your workouts or are they just more expensive? Have a real conversation with the person looking back at you in the mirror and assess two things: What are your shopping habits and reason you are in debt and how important is it for you to be debt free and financially independent? Only you can answer those questions truthfully. Do you buy things to satisfy a need? Are material things that you will eventually give away or throw away important to your overall happiness? If you fully commit to becoming financially independent, you will be able to pay off your debt and probably even more quickly than you expect because your mindset will shift.

Baby Step Three – Save three to six months of expenses in an emergency fund:

In and of itself, I think this one is very important. Everyone should have an emergency account, learn why here, with anywhere between three to six months worth of all of your expenses. This fund is for the “what ifs.” But where to put those funds is debatable. For almost everyone, I would suggest putting the funds in a high yield savings account. This allows that money to grow a bit but gives quick accessibility if and when it is needed. For the small percentage who want a fund that is more sophisticated, you might want to invest the money. My wife and I, at this time, invest our entire emergency fund, but that is subject to change if our situation dictates that change due to the ease and time of liquidity. I talk more about this in my YouTube video that you can check out here.

Currently since we have a healthy monthly cash flow, a six plus figure taxable brokerage account, over $30,000.00 in a health savings account (HSA) that we use tax free since we pay medical bills out of pocket, and cash in our checking account for our normal monthly bills, we decided to invest our emergency fund in a brokerage account versus a high yield savings account (HYSA). This is another area where I deviate from Ramsey. My contention is that personal finance is personal to one’s needs and current situation and not as fixed and rigid as is noted by Ramsey’s Baby Steps.

Baby Step Four – Invest fifteen percent of your household income in a retirement fund:

I am behind this one 100 percent and feel this is an absolute. I also support the amount that Ramsey suggests. If you invest early enough, which is as early as you possibly can, this is all you should really need. However, this also must take into account individual goals and thoughts on retiring. If you want to retire at an early age, you may need to increase the suggested fifteen percent to reach your goals. That is why I question and deviate from Ramsey’s one size fits all Baby Steps. Too often Ramsey’s method does not take into account personal goals and needs. Obviously you need to save whatever amount will get you to your end goal. Assess your goals and your investment time and adjust accordingly.

Baby Step Five – Saving for Children’s College Fund:

Here is another area where I totally agree with Ramsey. It is paramount to begin a college savings fund for your child or children early to ensure they will have enough money for college. Take into account rising expenses. My wife and I have a savings fund for Logan, our daughter, and will add to that if we have another child. Keep in mind that this does not necessarily have to be a savings fund for college. Instead, think about it as securing your child’s future which can include trade school and other forms of education and training beyond high school, purchasing cars, down payments on houses, or investing in a business venture. Regardless of what this looks like for your child beyond high school, investing in your child’s future is only wise. This has to be done strategically, investing early to allow the money to grow. However, your financial needs come before your children’s in the order of investing which is why this is Ramsey’s Baby Step Five. It is fundamentally imperative that you secure your finances first, so you will be able to invest for them. You do not want to rely on your children to have to take care of you financially when you are elderly. Therefore, invest for yourself and have your personal finances in order before you begin to invest for them. This sets you up for success, your children for financial independence, and eliminates you being a financial burden to them as a senior which is a loving act, not a selfish one. I have ideas and methods for investing for your children’s futures in one of my YouTube videos that you should check out here for further information.

Baby Step Six – Pay off your Home Mortgage EARLY:

By far, this is one of my favorite steps and one of the best pieces of advice. My wife and I bought into this concept and paid off our house as quickly as we could. There are many reasons to pay off your mortgage early. First, over and above the math, this is an incredibly freeing feeling not to owe the bank for your home. It is yours; you OWN it. There were math nerds who refuted our decision to pay off our mortgage, but our timing was impeccable. I know that most people can’t or won’t pay off their mortgages in two years and the market and interest rate won’t align like it did for us, so the math may work out to indicate that it is financially better to invest than to pay off your mortgage if you had to choose between the two. But that is the point. You do NOT have to choose; it is not an either or situation. Ramsey advocates this same notion. Think about having to pay your mortgage for your entire life AND think about what you are really paying for your home over those thirty years when you account for all of the interest paid. It is mindblowing. That is money you could have been investing. Now think about that but in reverse. How much money could you accrue over those years from the time your house was paid off and you were investing rather than paying? That is why my wife and I paid off our mortgage which we did before my wife and I were thirty years old. As long as you have followed the Baby Steps step-by-step, this is your next step, and it is a fundamental one. I can promise you this will be one of the most liberating and securing things you will do for your financial success.

Baby Step Seven – Build Wealth and Give:

I don’t think anyone can argue the need to build wealth nor can you argue the concept of giving. It is fulfilling, and I believe it is an obligation. That is why I am in agreement with Ramsey on this step. If you are at the point of building wealth, you should be financially secure. While you always need to be diligent about your finances and aware of your investments, by this point, you should not be worried about them. You should be able to live comfortably and well. Therefore, you should also be in a position to help those who need it. That is a wonderful gift and feeling.

Overall:

These are the Ramsey Baby Steps and how I align or disagree with each of them. The other thing Dave discusses is investing. Here is an area where we adamantly disagree. Before I delve into specifics where we disagree, here is a recap on areas where we are:

Invest 15% of your income. This is a variable amount, but in general, this is a good benchmark percentage.

Invest in a tax-advantaged retirement account. This is a good starting point, but you need to expand beyond this.

Diversify your investment portfolio.

Don’t chase your returns.

Invest for the long term.

So, what are the areas where I disagree with Ramsey? First, Ramsey advises investing in actively managed mutual funds, claiming he has had twelve percent returns compared to the average ten percent market return. This is absolutely not true. Perhaps he is speaking in gross terms, not net fees which is a big difference. Those following me know that is highly unlikely even net of returns. Also, Ramsey claims he falls within the one percent of people who “beat the market” and all those who follow his advice can also be in that elite group. I have shared plenty of reasons and stats why and how this is not the case.

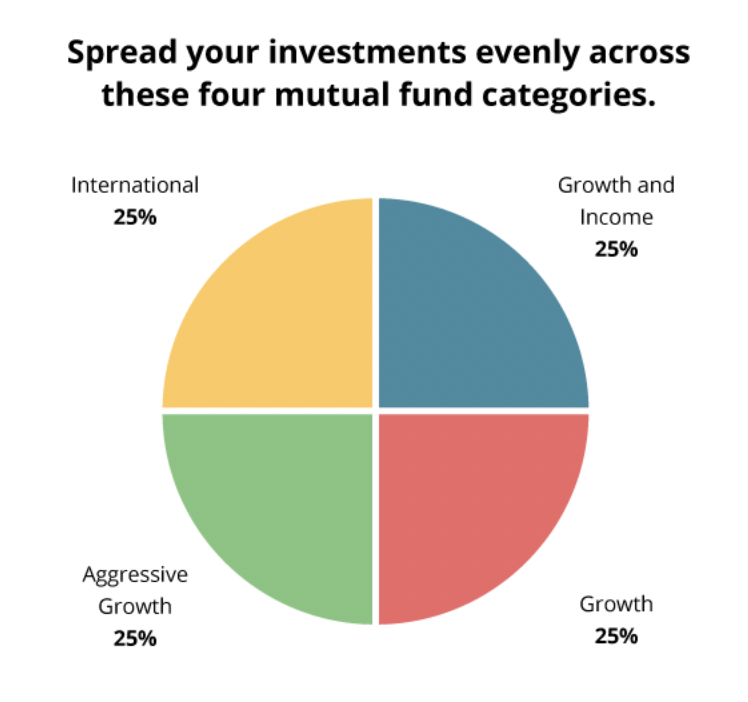

Another area where I deviate from Ramsey is in fund allocation. A four-way split allocating 25 percent for each category that is an unchanging and unwavering system does not make good financial sense. As your goals, risks, timeline, and lifestyle changes, so should your fund allocations. Ramsey contends that investors should equally divide funds between international, aggressive, growth, and growth and income mutual funds. I believe, on the other hand, that investors need to invest in low-cost index funds and Exchange-traded funds (ETFs). In addition, I am a firm believer in education and the importance of owning your own finances and portfolio. I don’t think it is necessary to use a financial advisor. You can get more information about this subject in my YouTube video that specifically covers that topic.

Regarding the Ramsey Group of Smart-Vestor “Pros” to whom Ramsey refers people, I personally tested them. What I discovered was that they were not fully vetted nor do they follow all of the advice as stipulated by Ramsey. In addition, as if that was not enough to cause me to be leary, they also charged a hefty rate for their advice and were less than enthusiastic or invested in me than I would have expected them to be. Keep in mind that Ramsey gets commission from this service and the Smart-Vestor Pros pay a fee to become part of his Ramsey network in order for them to grow their own businesses.

The last idea in which I deviate from Ramsey is that he advises against investing in individual stocks, whole life insurance, Bitcoin, annuities, Exchange-traded funds (ETFs), Certificate of Deposits (CDs), bonds, or Real estate investment trusts (REITs). But he does support investing in real estate if it is paid in full. Personally, I invest in a single stock which is META and also cryptocurrency, and the remainder of my portfolio consists largely of Index funds and ETFs. This is my personal approach as I have noted in my Investing 101 ebook.Despite what Ramsey advocates, my strategy is proven to be one of the most successful ways to invest and is also touted by investing giants such as Warren Buffet and Jack Bogle. I adamantly refute Ramsey in this regard because it does not make sound economical sense. However, with that said, I do agree that Whole Life Insurance and annuities are a racket and would not invest in them – ever. Today CDs also don’t make sense, but this can change quickly as interest rates change, so I would not say to never invest in them. Likewise, I think it is unwise to suggest that ETFs and REITs can’t be a good addition or part of a sound portfolio. Overall, investors have to be educated and make decisions that will meet his or her current and personal needs and wants.

Overall, I think some people are able to glean good information from Ramsey and his Seven Baby Steps. This, of course, depends on where you are financially. Ramsey has a simplistic, one size fits all, approach that has helped millions and can work to get people out of debt as outlined. Therefore, I am not dismissing what Ramsey has done or his method overall. It is all personal. You have to decide what you want your future to look like. How far will you grow your finances and what that will look like for you. Follow along with my story as I show you exactly how I am building wealth and teaching others to do it, too.

Many of you who have investments probably know that bonds traditionally have been considered a good investment, especially for those who like a diversified portfolio. The percentage of stocks to bonds and other forms of investments, including silver and gold, real estate, or cryptocurrency, is usually dependent upon the age of the investor and his or her risk tolerance. Since bonds are typically thought of as being fairly stable, more so than the stock market, many financial advisors and investors look to bonds as a must. Not only are bonds historically stable, they also yield an interest payment.

In today’s market, therefore, it seems like bonds would be something each investor would already have or would want to include in his or her portfolio, especially in light of today’s volatile stock market. However, the rising interest rates are driving bond prices down and yields up. This is due to bond prices being inversely correlated to their yields (Interest rate). As yields go up, bond prices come down. As yields come down, bond prices go up. Historically, the Federal Reserve would not be raising interest rates heading into a bear market, which occurs when a market experiences a prolonged drop in investment prices, but instead would be lowering interest rates to spur demand and stave off a recession. Today, the Fed is rightly more concerned with fighting inflation than the consequences of a recession.

So, what DO you invest in in Today’s market?!

Let’s jump into the fundamental differences between stocks and bonds so you can make the best decision for your portfolio. One differentiation is that when you buy stock in a company, you are buying a part of the company. This gives you, in essence, part ownership of that company, and, therefore, you ride out the good times with that company when there is a profit along with the hard times when the company is performing poorly and not yielding a good profit or maybe even suffering a loss. Bonds, on the other hand, is you, as the investor, providing a loan to a company or government, the borrower, which uses your money to fund its day-to-day operations and expenses. The result of this is that the investor receives interest on the amount invested in that company through the bond along with the original amount invested in the company or the government which is the principal amount. Since bonds are loans to a company, investors are paid regardless if there is a bankruptcy situation. Stock investors, however, are not ensured anything because they are “owners” of the company who profit along with or suffer from the highs and lows respectively of the company.

Bonds, therefore, are seen as fairly risk free, especially those issued by the federal government. However, while bonds are a good way to balance out a person’s portfolio, those that are considered lower risk usually pay a lower interest. The older the investor and/or the lower risk tolerance an investor has, the higher percent of bonds to stocks and other types of investments a person may consider in a diversified portfolio.

With the instability of the market, it gives all of us time to pause and evaluate our portfolios. We are hearing rumblings of the Federal Reserve raising interest rates again before the end of the year. Analysts warn investors against honing in on how many times the Federal Reserve raised the rate but rather how many points. The Federal Reserve is indicating that they plan to increase the rates by another 1.25 percentage points with the possibility for another hike after that.

Nonetheless, bonds along with stocks are not doing well. According to a report by the Associated Press, Federal Reserve Chairman Jerome Powell warned in August that “the Fed’s moves will ‘bring some pain’ to households and businesses” and that their “commitment to bringing inflation back down to its 2% target was ‘unconditional.’” Powell noted that he wished there was a less painful way to get inflation under control but “‘There isn’t.”

What all of this amounts to is that we are in for some serious volatility in the market. But that should not cause us to pull out of the market. Being diversified is still the best thing for your portfolio. Historically we know the numbers over the long haul. Personally, I will not be making any changes in my portfolio. I am not reactionary or an alarmist. I will continue to live by my budget and to invest, keeping in mind that there are always fluctuations in the market. Stay the course. Think through the best situation for you based on your age, your needs, and your risk tolerance and ignore the noise. Education is key – always. When you want to take your budgeting and finances to the next level and commit to making real changes in your finances and the financial outcomes in your life, contact me about Budgetdog Academy. Educate yourself and change your path to real financial freedom and independence. Continue to follow me at Budgetdog for all of your financial needs.

I am excited to announce that Vanguard is FINALLY rolling out fractional Exchange-Traded Funds (ETFs). What does that mean for you or other investors who want to purchase ETFs but want to keep investments to a specific dollar amount? Fractional shares allow a person to buy a portion of an ETF for any dollar amount, even as low as one dollar, rather than requiring the investor to purchase the entire share. So for all my Vanguard investors who focus on dollar cost averaging, fractional ETFs are now available to you. The only issue at this point in time is that while investors can buy fractional shares, investors cannot automate this process…yet! I did speak with a Vanguard employee, who said it should be “coming soon.” As soon as the automation component becomes available, I will be utilizing it and making some changes to my personal portfolio. I will shift all my current index funds into their equivalent ETFs.

This also enables investors to diversify their portfolios since they can invest in companies that might be out of reach financially due to the cost of the full ETF share. Other trading companies have offered this for some time, but now, Vanguard is adding this option to the services it provides.

When I first learned about this, I was concerned that this would cause a taxable event within non-retirement accounts. I verified with Vanguard that this would not be the case IF, in fact, the investor swaps his or her current index holding for the equivalent ETF. Since there is no taxable event and my fears have been allayed, as soon as they officially roll out the automation component, I will make this change. The adjustments that I will be making to my personal portfolio do not mean that I am changing my investment strategy in any way. My strategy remains unchanged. However, by utilizing these fractional ETFs, I will be able to slightly reduce the costs that are already minimal in my portfolio. I want to pause here and stress that this change to ETFs will have a small impact overall. I am attempting to maximize all of the benefits I can get.

Here are the main cost changes and things worthy to note in regard to ETFs:

Mutual Funds distribute capital gains to its shareholders, but Exchange-Traded Funds don’t. While Index funds are also mutual funds, they are passive in nature, and therefore, do not usually have a ton of turnover within. Therefore, capital gains distributions do not occur often for index funds. But it can, which is something I would like to eliminate if the choice was mine.

Expense ratios which indicate the cost of a particular mutual fund or ETF pay for the management, marketing, distribution, etc. of the portfolio. Within Vanguard, their ETFs are a few basis points cheaper than their equivalent index funds. It’s not much, but it’s still something.

Again, this is not earth shattering for most people but can slightly optimize your portfolio. Fractional ETFs open up opportunities to be more diversified and to purchase a variety of ETFs that may, otherwise, be out of the question due to the cost.

Vanguard has been beta testing fractional ETFs since December 2021, and it is now official. I will provide an update when they allow for automation for dollar cost averaging into ETFs. I did speak with them, and they said it should be “coming soon.” Stay tuned for more information about this as well as other breaking and helpful financial information. Follow me at Budgetdog.

In life, we are told to do our best, to win, and to succeed. It is odd to me, then, that when people do just that, we often criticize them or find reasons why they shouldn’t be successful and relish in the level they have achieved. I’m not about losing nor am I about to apologize for becoming successful. In fact, I want others to be equally or even more successful than me. That is why I created Budgetdog – not to see others flounder and suffer but to help them create plans to allow them to win. So how? How do you win and achieve success?

For the three plus years of owning my own business and working with thousands of clients, there are a few things that I have learned about winning. I have broken them down into five main categories. If you follow these, I am confident that you, too, will see success.

The first part about winning is Commitment. I have discovered that people who commit to their goals win. This is not a huge revelation. It just is true. The difference between my clients who reach their goals and win, thus becoming successful, is that they are committed. They marry themselves to the idea of winning. It is important to keep the goal in mind and to stay true to that goal, never wavering and making changes but rather to live out the goal. They are steadfast and resolute, understanding the time to start is right then, not sometime in the future or when things will be easier or better or more convenient. If you really want to win, you will make the commitment and stay true to it, accepting nothing less and making no excuses.

The second key component to being successful is finding a Mentor. It is imperative to find someone who has done what you want to do. This person will be invaluable to you. Human-decision-making fascinates me. Why? Because it seems like it only makes sense to find a mentor, yet the average person is so desperate to want the quick and easy way to success, that this component never seems to enter into the picture. Moreover, instead of learning from a mentor who knows all of the pitfalls and difficulties, many people who just want the quick and easy way will fall prey to anyone who makes alluring false promises. Just like with setting goals, you need to find someone who actually is successful and learn from that person. Ask questions, seek help, have frequent conversations, learn how to win and be successful completely and truly, not just for the immediate, and, most importantly, make sure you have the right mentor. For example, from my experience, my clients fall into four different groups: those who want to get out of debt, those who want to become millionaires, those who want to build a business, and those who want to quit a nine to five job. I have done all of these things. Therefore, I can successfully be a mentor to someone who wants to achieve one or more of these goals. I have the blueprint and the experience to help guide in any of these areas, so my clients are able to win and be successful. However, if someone sought me out to be a mentor for trading, I would not be the right person to adequately help him or her since that is not my area. I only speak about what I know and about areas in which I am personally successful. But it is not always that way. Many contend they can give you all kinds of advice and can help you along your way to success, but they don’t actually have the background and the personal experience, so be wary of who you trust with your success.

Another key aspect of winning for success is Hunger. You have to REALLY want something with every fiber of your being in order to be truly successful – not kind of want it or want it a little – but really passionately be hungry for it. Tony Robbins, a leading author, speaker, philanthropist, and life and business strategist notes that there are many ingredients to success, but one key element that pushes you to achieve it is hunger. Robbins said, “Hunger will destroy that fear of failure. Hunger will drive you through it. Hunger will be your resolve. It is the force that locks you into a commitment, it fastens you to the outcome when you’ve decided upon a result and you won’t sleep at night until you achieve it. Hunger is irrepressible.” It is far greater than passion. Hunger fuels all of the other essential elements that you need to be successful including vision, discipline, consistency, relentlessness, curiosity, and courage. If you don’t have hunger, you will not win so don’t waste your time. You don’t really want it bad enough and are not committed enough to throw everything at your goals, your desires, your hopes, and your dreams if you aren’t passionately and fervently hungry.

To be successful and to win, you also have to dare to be Different. This is the fourth component to success. Dare to go against the norm, to break away from the mold, and to allow yourself not to be average. Self-awareness is key. Are you that person who is strong enough and self-assured enough to be different? Look around at the masses. Note what they do every day including for many of them living mundane lives in jobs they hate. Just because so many others live that way, does not mean it is right for you. Don’t settle. If you do what everyone else does and it is average, know that you will get the same results, and it will be just that – average.

The last component to success is Mental Toughness. Winning is not going to be easy, nor is success. It is going to be hard, and you are going to have to sacrifice in order to achieve your goals. That is why so many others fail. It is difficult to see past the easy and the immediate. If you want it now, want the easy way, you will lose – guaranteed. It is going to take hard work, sacrifice, time, commitment, passion, and a desire or hunger that goes beyond what most people are even capable of thinking, feeling, and doing. Sure, your skills and knowledge are important, but if you can’t work through adversity, you will never win. Know that your resolve is going to be tested, but you have to be willing to take the jeers and the jabs in order to be successful. And you have to keep getting up, bracing yourself for more, and taking all of the setbacks. With each setback, you can’t think of failure but rather of a learning experience.

I am happy to mentor you on your way to success, but you are the one who has to be hungry enough, passionately and thoroughly, to really want to make it happen. You have to have the strength, the desire, and the resiliency to be in for the long haul. Keep all of these components in mind and live them – fully and completely. I hope you dare to be different and to seek to win. Believe in yourself and dare. It is a great place when you get there, but it is not fast or easy. Reach out to me for help and guidance.

Regardless of whether you already have an IRA or are interested and in need of getting an IRA, this blog will provide some helpful information to better understand this investment account.

To begin, I want to break down two common misconceptions about IRAs. First, let me dispel the idea that an IRA in and of itself is the investment. It absolutely is not. It is just the vehicle that contains different types of investments such as mutual funds, index funds, stocks, bonds, and REITs. You need to understand this to better understand your own IRA and to know exactly where your money is invested. Don’t be misled into thinking an IRA is THE investment.

The second misconception is that an investor can NOT touch his or her money until age 59 and a half. That is not exactly true. You may withdraw contributions from a Roth IRA at any time tax and penalty free. But in order to withdraw contributions penalty free, you must follow one of the two rules:

The Roth Conversion Ladder:

A Roth IRA Conversion Ladder entails moving your money from a tax-deferred account, such as a 401k or Traditional IRA, into a Roth IRA. The benefit is that it allows you to withdraw the converted funds from your Roth IRA after only five years.

The Rule 72(t):

Rule 72(t) permits you to establish a schedule of annual or more frequent withdrawals from your retirement account called SEPPs (substantially equal periodic payments). When you withdraw money from a qualified retirement account under Rule 72(t), the funds are distributed to you as SEPPs. These regular payments are made over the course of five years OR until you turn 59½.

If you have interest in one of these two routes, I highly recommend working with a CPA to ensure accuracy and completeness (why does this remind me of Deloitte auditing assertions? haha)

Now let’s dive into some additional facts about IRAs.

First, understand that you are not permitted to keep funds indefinitely in a Traditional IRA. You will need to take minimum distributions known as RMDs when you reach 70½ unless you were born after July 1, 2019. If you are born after that date, you will not have to take RMDs until you reach 72 as per the Secure Act.

Another important concept about IRAs is that there are two types which often confuses people. Simplistically, the difference between the two, a Roth IRA and a Traditional IRA, is when you will pay taxes. If you want to pay the taxes initially, you would invest in a Roth IRA compared to paying taxes later which you would do with a Traditional IRA.

So which is the best investment for you? This is not a clear cut answer, but one that is unique to each investor as based on his or her financial situation. Let’s break this down to the basics to make some sense of what is best for you. The general rule is that if your income tax bracket is going to increase in the future, you will want to invest in a Roth IRA; you should choose a Traditional IRA if your income tax bracket will decrease in the future. So assess your personal financial situation before deciding which type of IRA is best for you. Again, that is the general rule as of today, but that is always subject to change, and it is difficult to determine a person’s income in thirty or so years. Think about when you want to pay the tax. Do you want to pay on the initial investment now, or do you want to wait and pay later on the compound growth of your investment?

Roth IRAs also carry some income limits which investors need to understand. I think that whenever the Government attaches restrictions, you need to be alerted to the reasons why. The income limits known as MAGI for the Roth IRA in 2022 were as follows:

Single – $129,000.00 which phases out at $144,000.00

Married Filing Joint – $204,000.00 which phases out at $214,000.00

You will need to assess your financial situation to determine what is best for you, but if your MAGI is below these limits, I would strongly consider investing in a Roth IRA. However, if you do go above these limits, you can still take advantage with a Backdoor Roth IRA. Wealthy people often utilize this investment strategy which is perfectly legal, just a bit unconventional and less well known. A Backdoor Roth IRA means you invest in a Traditional IRA and then convert that invested money into a Roth IRA. Not only is this method employed by those who are wealthy but also by those who have a Traditional 401k who want to split pretax and post-tax money.

Since it is not a black and white, clear, and easy decision between a Traditional pre-tax or a Roth post-tax IRA, many times there needs to be a combination approach. On a personal note, this is what I do. You will need to consult with a CPA you trust and who is well-versed to help determine what is best for your financial situation.

The good news is that you are able to recharacterize IRA contributions in order to change the initial designation. So, for example, if you made contributions in a Roth IRA and then realize you exceeded the Roth IRA income limits, you may recharacterize it to a Traditional IRA contribution.

To determine which IRA is best for you and your retirement, you will need to calculate your GROSS annual income. It is commonly recommended to invest about 15% of your gross annual income into retirement. Good steps to follow for where to allocate your 15% are:

Invest up to the limit of a 401k company match if offered

Max out your IRA

Invest the remaining portion into a 401k

Let’s take a look to see how that looks with numbers. We will use a 3% company match for our calculations and an annual gross income of $100,000.00.

$3,000.00 for the company match ($100,000.00 X 3%)

$6,000.00 (IRA limit for 2022)

$6,000.00 invested in a 401k which is the remaining to reach 15%

The end annual result is that you are investing $6,000.00 into an IRA and $9,000.00 annually into a 401k. I would split the $15,000.00 investment dollars into bi-weekly payments throughout the year and would have all of the payments set up on an automatic payment system for ease. I would also recommend that you offset the IRA with the 401k. Preferably consider staggering your payments with your income payout dates. Therefore, if your payroll is on the first and third Fridays or days of the month, it is best to automatically invest in your IRA on the second and fourth Friday or day of the month that corresponds to the payday.

Again, let me reiterate that this is the general rule of thumb for retirement, but you may have different retirement needs to keep in mind. It is best to work with a certified financial planner or CPA to help guide you through this process. Reach out to me for additional help with your retirement questions or with any questions about finances, budgeting, and investing. Remember to follow me @Budgetdog on Twitter, YouTube, Facebook, and Instagram for daily financial content and education.

My question to you is what Motivates you and is your Passion? Passion is not a job. Rethink your answer if you assumed it is the same thing. Also, rethink the tangible and the intangible. I am talking from experience and misconstrued priorities. I believed what I had been taught that tangible things and status would make me happy. These were things I was brought up to believe were the end-all. I quickly, but not soon enough, came to realize how wrong this message is. So, if you are trying to set the world on fire and climb the social ladder for status and success and think this will bring you happiness and contentment, please read this and think about your priorities and your passions.

I am going to step back to my younger self who was confident that I had made it and knew all of the answers. I am a planner, so I thought I had reached the pinnacle when I graduated college with an accounting degree, secured a job with Deloitte, was working to pass my CPA exam, had gotten married to my long-time girlfriend, and was on my way to making partner – all as I had planned. My wife and I thought I would climb my way up the corporate ladder for about 40 years, have a couple of children, and live happily and contentedly ever after. I was not only wrong, but I was disenchanted. I had bought into a false narrative. I also realized that my plans did not play out as smoothly and as easily as I had expected. Just because I wrote it down, didn’t mean it came to fruition. Wow! This was mind-blowing and unexpected.

First, I hit a brick wall with the CPA exam. I did pass it eventually, but it was an arduous two-year long undertaking which was also very humbling. Still, my wife and I plowed ahead – AS PLANNED. Remember, I was going to climb the corporate ladder and become a partner at Deloitte which would create bliss and be the answer to everything. I wrongly thought reaching the level of being a partner would make our lives so easy. Shortly after getting my CPA, I had an epiphany about all of this. In retrospect, I wonder why I was thinking EASY was the right way and the best way and why I was so consumed with income and status. With a new mindset, my wife and I paid off $76,000.00 of non-related mortgage debt and were undertaking the process of paying off our mortgage at breakneck speed.

So, what was the epiphany that changed my perspective? According to my PLAN, the thing that drove me was to become a partner in the company, have my wife stay home to raise our children, and relish in the status and affluence that came with climbing the social ladder. There is nothing wrong with this plan EXCEPT this would NEVER have brought me happiness and was only what I was striving for because I did not really understand passion nor did I have my priorities straight. Quite honestly, my EGO was what was driving me. I was worried about my reputation and my ego blinded me.

It wasn’t until one late night when I was doing an audit which was going to continue into the wee hours of the morning when my colleague, who was also striving to become a partner and had been clawing his way to the top of a daunting list for a long time, called his children to say good night. At that moment, I KNEW to the depths of my being that this life was not for me. What is the price of success? If not being fully present in my family’s life was the price for “status” and “success” as deemed by the masses, then I was out. I was not and am not willing to sacrifice time and experiences with my wife and our daughter to be a partner in any corporation or for anything else.

What an interesting concept – success. How do we define success? What is our passion? Are things more important than time with our loved ones? What is the price we are willing to pay to kiss our child or children and spouse good night? For me, there was no price. I knew when my colleague made that call that I would never pay the price of time with my family like that to be deemed “successful” according to society. Moreover, it also gave me pause to realize that my side hobby of helping others with their financial journeys was my real passion. It no longer mattered to me if it would be that lucrative, but I was certain it would be more fulfilling and that it would afford me precious time with my family. It would also allow me the freedom to reach the heights I wanted to reach without having to be a sycophant, feeling like a puppet in a costume trying to impress the higher-ups and groveling for any accolades that came my way.

That is how Budgetdog came to be. Some of you have heard my story of Budgetdog before, but it was at that moment, late at night in a gloomy office, when I decided that that life was not for me. I knew I needed more but not in the way society dictates or that our culture tells us is good and right. I have remained steadfast in my journey since that day to follow my passion and to align my priorities to what is helpful and good – not financially but moralistically – despite the fact that I didn’t even make a penny for the first sixteen months of its beginning. What began as my passion to help people and an attempt to find something more meaningful than my existence doing the same meaningless and rote job even amidst the gibes at a bachelor party in Las Vegas as my friends taunted me with “Budgetdog, Budgetdog, Budgetdog” is a life that affords me the time and ability to live life fully.

I remain resolute in my decision. I understand the difference between a job and one’s passion or mission. What began as a hobby and a desire to help others is now my full time endeavor. To date, I have aided countless to improve their lives financially and perhaps even emotionally by helping them alleviate undo financial stress. What is the price for that? There is not a price tag that I can put on it.The jeers did not and do not bother me. I am no longer a coward with a misplaced ego. Even when a Deloitte partner mocked me when I gave my two week notice as I told him about Budgetdog, I was not daunted. Laugh! That is fine. Now I have the last laugh. I am living a life of freedom and passion.

Think about your priorities – not those of others or of society. Often those are flawed. My priority is to my family. I quit my job a month before my daughter, Logan, was born. Her birth has even more profoundly changed my priorities. Partner? No thanks. Possessions? I don’t need or want them. Staying home, being with my baby girl is my priority. At all costs, our lives are about our families, not status which is such a subjective rating. Interestingly, our daughter was born with a rare genetic mutation called Dravet Syndrome which means constant care and monitoring as well as endless doctor visits, trips to the ER, and other things that are time-consuming that go beyond the normal scope of parenting. How blessed am I that I made the choice that I did, so I am able to be the caregiver for her. I can’t ever imagine putting work ahead of her needs. Life is too short and my time with my wife and daughter is worth more than anything. That is my passion, motivation, and priority.

So, I challenge you to assess where you are and to ask yourself the tough questions. Don’t define yourself by false definitions or what society has instilled as what you need and want. What are you willing to sacrifice and for what? This is truly personal. For me, time and freedom are more important than money and possessions. Of course, we need money to live, but how much and at what expense? Only you can answer that. Finally, don’t be surprised that when you do find your passion and trust your abilities, that you won’t exceed your expectations and that of others. I know I have but that was not the point. Passion and Priorities are!

I am going to deviate from my norm for this blog of all things financial and talk about life – real life, not an Instagram World or a world of selfies and posed pictures or a life that is staged to look all perfect and wonderful. No, this is the real world with all the bumps, bruises, and imperfections that go along with it. Don’t misconstrue my message. I am not complaining but rather telling you how I live in the real world. Along with this message, let me also express that I know I am blessed and feel so fortunate to have such an amazing and devoted wife and the most wonderful and beautiful daughter that a dad could ever dream of having. But, again, all of this is real. So, this blog is more a look into my real life, my life behind Budgetdog with its blogs, Twitter and Instagram, and all of my podcasts. This is about my real life as a dad to my daughter who is turning one and the journey she has taken us on over the last months.

First, I want to say Happy Birthday to my precious baby who turned one on September 4th. What a joy she is and what a worry at the same time. Some of you who know me intimately, know that prior to January 29, 2022, our lives were better than we could ever have imagined or dreamed of financially, emotionally, and personally. Of course, we had some ups and downs and some bumps like everyone, such as car and appliance repairs and other “normal” life things. But nothing earth shattering or devastating. For that, we were lucky and had worked hard to achieve it.

Then on January 29, 2022, our whole world was turned upside down and inside out to the point that it is still raw and surreal. On that day, our seemingly healthy baby suffered her first seizure. It is beyond an understatement to say that it devastated us. Imagine my horror when Erin, my wife, came running hysterically into the room where I was preparing to make a company presentation, shaking and saying that something was terribly wrong with our baby. As most who suffer some type of shocking event or trauma, I still can remember every minute detail from that experience and relive it over and over in slow motion.

After arriving at the emergency room and having Logan evaluated, we were reassured that babies having seizures is not that uncommon and were discharged. We left the hospital, feeling somewhat better but still frightened only to return by ambulance exactly twenty-four hours later with another seizure. We kept wondering if this too was “normal” as our minds were a whirlwind of incoherent and jumbled thoughts. In one day’s time, our lives changed forever.

That became our first of many hospital stays, lasting four days but providing few answers. Questions plagued us. Finally, after a battery of tests, they were ready to dismiss us with little information other than things seemed to be okay. As we were preparing to leave, a doctor came back in, telling us they noticed something on the EEGs that did not seem “right.” What did that even mean? We were sickened by so many medical terms, so many questions, and so many incoherent thoughts that we were trying to absorb.

Since that fateful day, we have had too many ambulance runs to the ER and too many hospital stays. Eight full months into the year, our total hospital bills have soared past $150,000! We know too many of the amazing nurses in the Neurology unit at Cincinnati Children’s Hospital and the EMTs who all seem to know the drill all too well when they get the familiar calls to our house.

We have also finally learned, through a series of wonderful and oddly strange events that have opened doors and have put us in touch with the right doctors, that Logan has Dravet Syndrome. In one fell swoop, our daughter who appeared to be perfectly healthy was diagnosed with this rare syndrome that affects one in every 15,700 children. Like all syndromes, it presents itself differently in each child. Some children have mild and even few seizures, complications, and side effects, but others have many severe seizures and complications including lags or regression in mental and physical development and even death in extreme cases which is about 15 to 20% of those diagnosed with Dravet Syndrome. There is currently no cure for Dravet Syndrome. There is active research in the field given doctors are aware precisely the gene that is the main cause (SCN1A). We are hopeful with time that a miracle surfaces. What about Logan? We have so many questions and no answers or guarantees. But isn’t that all part of living in the real world?

It is not only the diagnosis and the unknown that make life so difficult, but for children like Logan and the families, it is the minute-by-minute worries rather than the day-to-day struggles that are difficult to handle and absorb. For us, life with Logan is like living with a ticking bomb. Daily life is arduous. Typically life with a baby, a child, or children is hectic and busy. We would gladly welcome that. That was what we were expecting. Instead, we are always living under the shadow of another seizure which leads to more complications and problems.

Logan comes with a long list of dos and don’ts that amount to our daily tasks being overwhelming as they consume our time and energy. Some of our struggles with Logan which are the same with other children with Dravet Syndrome are that she can’t get overheated or have rapid changes of temperatures, overstimulated or overexcited, or overtired or sick. That eliminates so many things such as going outside, even for a simple walk in the stroller on most days. Photosensitivity is a trigger for some with Dravet Syndrome, so we err on the side of caution and try to keep Logan out of the sun too much, vying for shade whenever possible. If she is out in the sun, she has to have her eyes shielded. Try keeping sunglasses on a baby! It is almost impossible, but mandatory. Water is another trigger due to the overstimulation and temperature change. Obviously, going to a pool is out, but it also makes bathtime a worry. For most babies, bathtime is such a fun time. But for us, it is a time when we have to be guarded and alert. The water has to be carefully regulated, and we can’t allow her to get overstimulated or over excited. So, a seemingly fun and easy daily routine for us is one that is filled with trepidation. In addition, for the average parent, a missed nap leaves them with a cranky baby. For us, it is catastrophic and one that almost always leads to a nasty seizure. Each nap and sleep session has to be carefully calculated to ensure that she is getting enough sleep throughout the day and night. Unfortunately, Logan is not able to relax enough to allow herself to fall asleep and stay asleep. We have spent countless hours trying to remedy this, including working with sleep specialists. She sleeps in a SlumberPod when we can’t be home that resembles a tent or in our pitch black bedroom closet always with white noise all in an attempt – and often a futile one at that – to help her get some sleep. In addition, during any time when she is sleeping, Logan is hooked up to a variety of monitors including one that detects rapid movements that would indicate a seizure, an oxygen monitor to allow us to be alerted if she stops breathing, and a sound and visual monitor to help us watch her as she sleeps – or tries to sleep.

Daily life and normal routines are a worry. Every activity of every day must be carefully checked. As mentioned, Logan and those like her don’t regulate excitement and stress like other children and people. This overstimulation includes but is not limited to sounds, different movements, and quick motions. Just dropping something which makes a louder than normal sound or a flash of light is a worry. Even sitting on the floor playing with her is different than it is for most babies and children. We are ALWAYS watching and asking ourselves if her movement was a normal jerk or twitch or if it was a myoclonic seizure. We are constantly assessing whether she can keep playing or whether we need to pick her up and try to calm her to prevent a seizure. There are so many triggers for her seizures, but they are all such a part of everyday life that most people don’t even give them a thought or a glance. For each of these events, we hold our breaths and prepare ourselves for another seizure, rescue meds, and the chaos that ensues after.

Furthermore, excitement and exciting things are a fundamental and normal part of development and growth for all of us. Our constant struggle is how to help her grow and develop, learning new things and experiencing life and all of its wonder and beauty while at the same time, eliminating the triggers. With each new phase and discovery, we brace ourselves as we await a sleeping dragon to rear its ugly head in the form of a seizure. We live our lives in a state of hypervigilance in order to safeguard Logan from the many triggers that plague her. Because of this, we have had to isolate ourselves and Logan. We can’t go out, have missed many family events, and rarely are even able to see our immediate families. This also means they are not able to see Logan or engage with her. But it is not about us. We all know it is about Logan.

Logan’s constant monitoring is a reality; it is our responsibility and our lives. The more we can lessen the seizures, the better it is for Logan. Watching your child go through something like this is beyond words. It is crushing. Being able to stay home with Logan has been a blessing. Budgetdog has enabled me to be there with her to monitor as many of the activities and situations as possible. If it had not been for that, one of us would have had to quit a “day job” to stay home. I can’t imagine trying to handle the stress of a financial worry on top of all of the anxiety we already have. But that is where we are, and we count those blessings.

So, today and each day, we celebrate Logan where she is, and we know that she is perfect no matter what her perfect looks like. We are deeply committed to providing the best possible care we can for her including the most up-to-date and effective medicines and therapies available. We have immersed ourselves in learning everything we can about Dravet Syndrome and are trying to bring awareness about this syndrome to everyone we can. In one short year, Logan has totally changed our lives. This is real. It is not always pretty or easy, but it is life as it is.

For parents, there is no way to imagine loving a child anymore than you do. Parents love their children unconditionally, wholeheartedly, and purely to a level that is like no other love. Logan has taught us in this first year, how to be totally selfless and more appreciative for all of the blessings in life as well as how not to take anything for granted. Living in the real world with . Logan is unimaginably challenging but so remarkably rewarding and incredible. We know how blessed we are to be the parents of such an amazing daughter.

Happy Birthday to my baby girl. We pray that we can celebrate many more birthdays and cherish each moment of your life. We also pray for all of the parents and children impacted by Dravet Syndrome and other syndromes like this. It is our mission to find cures to help all of the Logans out there.

For more information about Dravet Syndrome and the research that is being done, check out https://dravetfoundation.org/.

Our goal is to donate $1M to Dravet Syndrome and you can help HERE!

I do not usually do this, but if you can…please share this blog and help us bring awareness to this very rare disease! You can tag me on all social medias. Thank you from the bottom of my heart!

In today’s economy, we are all scrambling to ensure that our investments are making as much money as possible. We expect fluctuation in the market but need to make wise choices when deciding what we should have in our portfolios. Historically, for twenty years up to December 31, 2021, the S&P 500 Index averaged 9.5% per year, but the average equity fund investor earned a return of only 3.9%. Investors are always trying to beat the market and to time the market, and they continue to lose. Index fund investing has proven over time to be the most successful way to win in the market. I’m here to give you some advice about the top five index funds that you may want to consider for your investment portfolio. Keep in mind that the number of stocks in each fund as well as the top stocks fluctuate along with the market. Therefore, the information used in this blog may not be exact at the moment you are reading this blog. I encourage to check the latest data for each fund to see the changes.

Top Five Index Funds:

I work with Vanguard; they are the one with whom I have my investments and are my top picks. Please note that if you already have investments with Charles Schwab or Fidelity, you can buy equivalent funds to the ones I am suggesting, but I would not recommend buying the Vanguard funds I am recommending through another broker due to the fees you would incur. Reach out to me individually if you are working with a different broker and need help figuring out what the equivalent to the Vanguard funds I am discussing here or download my free investment fund cheat sheet here.

#1 – Vanguard Total Stock Market Index Fund (VTSAX) –

Vanguard Total Stock Market Index Fund is an index fund that tracks the entire United State equity market, thus providing investors with exposure to virtually the entire United States stock market which includes a variety of 4,076 small-cap, mid-cap, and large-cap stocks according to Vanguard as of July 31, 2022. The fund’s top five stocks reported by Vanguard as of July 31, 2022 are Apple, Amazon, Google Class A, Google Class C, and Microsoft Corp. Since the United States makes up 50% of the global market, this is a very attractive fund. In addition, it has an expense ratio of 0.04% which means you only pay $4.00 for every $10,000.00 invested. My guideline on a personal level in this regard is that I never go above 0.20% or twenty basis points. Basically you can invest in this stock for almost no cost. My portfolio consists of 73% VTSAX.

#2 – Vanguard 500 Index Fund (VFIAX) –

Similar to my #1 pick, the Vanguard 500 Index Fund is also an index tracking fund and it also has an expense ratio of four basis points. One big difference is that this fund covers the top 500 United States companies, so you get the majority of the domestic market with this fund. While it is labeled as Vanguard 500, there are really 503 holdings due to parent companies such as Alphabet which is actually Google’s parent company, dividing out class A and class C shares according to Vanguard as of July 31, 2022. Another difference between Vanguard Total Stock Market Index Fund Admiral Shares (VTSAX) and this fund is that you only get the large-cap exposure. The top five stocks in VFIAX, like with VTSAX, are Apple, Microsoft, Amazon, Tesla and Google as noted by Vanguard’s latest data. VTSAX has 4,076 stocks while VFIAX only holds 503 stocks, but the S&P makes up 80% of the United States market. Because of the vast similarities of the two, however, I would choose one or the other, and my preference as noted above is VTSAX.

#3 – Vanguard Total International Stock Index Fund (VTIAX) –

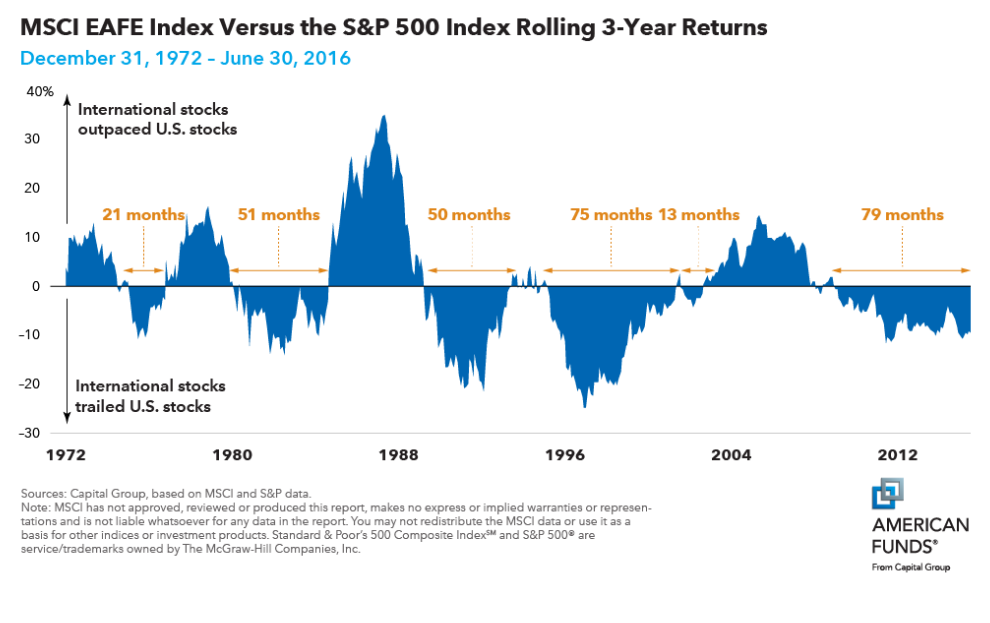

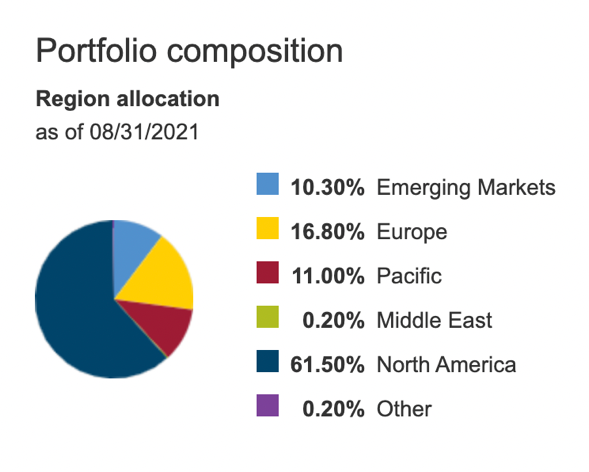

My third preference is the Vanguard Total International Stock Index Fund which is an index fund that provides investors the luxury of investing in developing as well as emerging international economies. Despite the fact that the United States makes up 50% of the global economy, there are many thriving international companies. This fund has a higher expense ratio than the first two picks with eleven basis points which is still below my guideline and is good considering that you will only pay $11.00 for every $10,000.00 invested. According to the latest data by Vanguard dated 7/31/22, there are 7, 819 stocks in this fund from Europe, the Pacific, the Middle East, emerging markets, and even some from North America. Vanguard has noted the top five stocks included in this fund are Taiwan Semiconductor Manufacturing Co. Ltd., Toyota Motor Corp., Shell plc., Tencent Holdings Ltd.and Samsung Electronics Co. Ltd. Just as the number of stocks in the fund changes, so do the stocks within the fund. The beauty of this fund is that it helps round out your portfolio which as a global investor I think is important. However, be aware that since this fund invests in stocks that are from around the globe, including those that are in developed as well as from emerging markets, this fund can have more volatility than you may see in a domestic fund along with political risks and currency risks. You may want to assess your financial personality and level of risk to see if this fits your investing tolerance profile before including it in your portfolio. For me, I think excluding the other 50% of the world seems shortsighted, especially taking into account that the United States and other countries have historically and continue to vie for the top financial spots. For that reason, 19% of my portfolio consists of this fund.

Following is a chart that indicates how often international stocks have outperformed United States stocks and solidifies why it makes sense to me to invest some of my money in these stocks.

#4 – Vanguard Emerging Markets Stock Index Fund (VEMAX) –